Are you planning to buy a residential property soon? Or thinking of finally having your permanent home built? With a growing family, this has been on my and my husband’s minds for a year now. We invested on a lot back in 2013 and now we’re ready to have a house built on it. While it’s easy to say, “Let’s build our house now!” –it’s easier said than done. We also have to think about how we’re going to finance the development. That said, we’re currently researching on the best housing loan interest rates in the Philippines offered by some of the most trusted banks in the country.

While some would say not to take out a loan and to just save up for something you want, we don’t think it applies to having a house built. This isn’t just a 100k spend that you can save up for in a year. Saving up for a house will cost much more–and honestly, we don’t have the time to wait that long. Renting is no longer an option for us, we want a permanent home.

Housing Loan Interest Rates in the Philippines

That said, our option now is to take out a housing loan payable for 10-15 years from a bank that offers the best interest rates.

If you’re planning the same thing, here’s some helpful information from Lamudi Philippines, a leading global property portal for sellers, buyers, landlords, and renters. Lamudi was established in 2013 in Berlin, Germany, and it is currently available in Asia (the Philippines, Bangladesh, Indonesia, Myanmar, Pakistan, and Sri Lanka), Latin America (Mexico, Colombia, and Peru), and the Middle East (Jordan, Qatar, Saudi Arabia, and the United Arab Emirates), and MyProperty.ph, the leading website in the Philippines with listings of pre-selling properties and properties for sale and for rent, and also provides relevant and updated industry news and information for its clients and consumers.

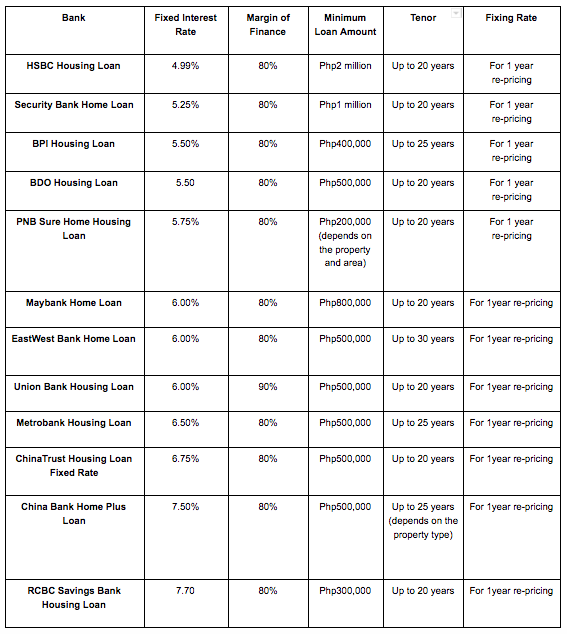

To help you decide, here’s a list of housing loan interest rates in the Philippines:

Terms You Need To Know

Fixing Rate

In addition to interest rates, it is equally important to note the loan tenor of the fixed rate that you are agreeing to. All interest rates given in the table provided below falls under the one-year re-pricing period, this means that interest rates are subject to change per year. Although price change does not necessarily mean that rates will go up, it is still crucial to know and expect that your amortization fees will vary each year depending on the current interest rates.

Banks also offer a fixed interest rate for a longer span, the longer the tenor, the higher the interest. For example, BDO offers a fixed 6.5 percent interest rate for a length of two to three years and 6.88 percent fixed interest rate for a four to five years duration.

Margin of Finance

Most banks can lend up to 80 percent of the property’s selling price, while the remaining 20 percent will then be paid as equity or down-payment directly to the developer or the seller.

Among all banks listed in MyProperty’s comparison, only Union Bank can lend up to a maximum of 90 percent of the property’s selling price. This is good news to some homebuyers who do not have enough cash to cover a 20 percent down-payment.

Loan Tenor

Unlike the government shelter agency Pag-IBIG Fund who offers loan tenors of up to 30 years, banks’ normal maximum loan tenor is only 20 years. Some extended their offering up to 25 years, while only EastWest Bank follows the model of the government bureau for offering 30 years tenure. Although paying in longer duration means your total payment will be higher, this helps lower monthly mortgage payments, which might be more manageable to some borrowers.

Fees and Charges

Miscellaneous charges vary from the requirements of each bank, but homebuyers must expect and be ready to spare some cash to cover these fees. Some of the common additional expenses included when applying for a housing loan are appraisal fee, registration, documentary stamp (Php1 for every Php200 of the loan amount), and notarial fee.

Mortgage Redemption Insurance

When applying for a housing loan, the bank or lender will normally ask the borrower to get a mortgage redemption insurance or MRI, which is a form of life insurance that pays off a part or the whole of the insured’s outstanding mortgage balance in case of his or her death or total disability. MRI guarantees the bank that it will be paid back the amount it has lent, and also protects the borrower’s surviving family, as it will help settle the outstanding housing loan amounts. In the absence of an MRI, the bank or lender may sequester the house from the surviving family. The MRI is usually incorporated to the housing loan in lump-sum payment (one-time premium paid annually).

—

Hopefully you found this article helpful! If you have any questions or advice to soon-to-be homeowners, feel free to leave a message in the Comments Section below.